If you’ve been working in accounting or preparing financial statements, you’ve probably seen items that look like assets but don’t actually have real value. Many professionals still get confused about how to treat them correctly. In this guide, we explain fictitious assets in simple terms, with UAE-focused examples and practical accounting treatment.

Key Takeaways

- Fictitious assets represent expenses or losses not fully written off in one period

- They have no physical existence or resale value

- Common examples include preliminary expenses and share issue discounts

- IFRS does not recognize fictitious assets as real assets

- Proper accounting improves compliance and financial clarity

- UAE businesses must follow IFRS for reporting

What Is Fictitious Assets?

Fictitious assets are expenses or losses that are not completely written off during the accounting period and are temporarily shown on the asset side of the balance sheet.

These assets do not have any real value and cannot be converted into cash. For example, preliminary expenses during company formation may be spread across multiple years instead of being expensed immediately.

They are recorded to reduce the burden of expenses in a single year. However, modern accounting standards discourage this practice.

Why Fictitious Assets Matter

Fictitious assets matter because they affect how profits and financial positions are presented.

Spreading expenses over time can make profits appear higher in the short term. For example, instead of showing AED 100,000 expense in one year, a company may spread it over five years.

This impacts transparency. UAE businesses must follow IFRS, which requires accurate and fair financial reporting.

What Are Common Examples of Fictitious Assets?

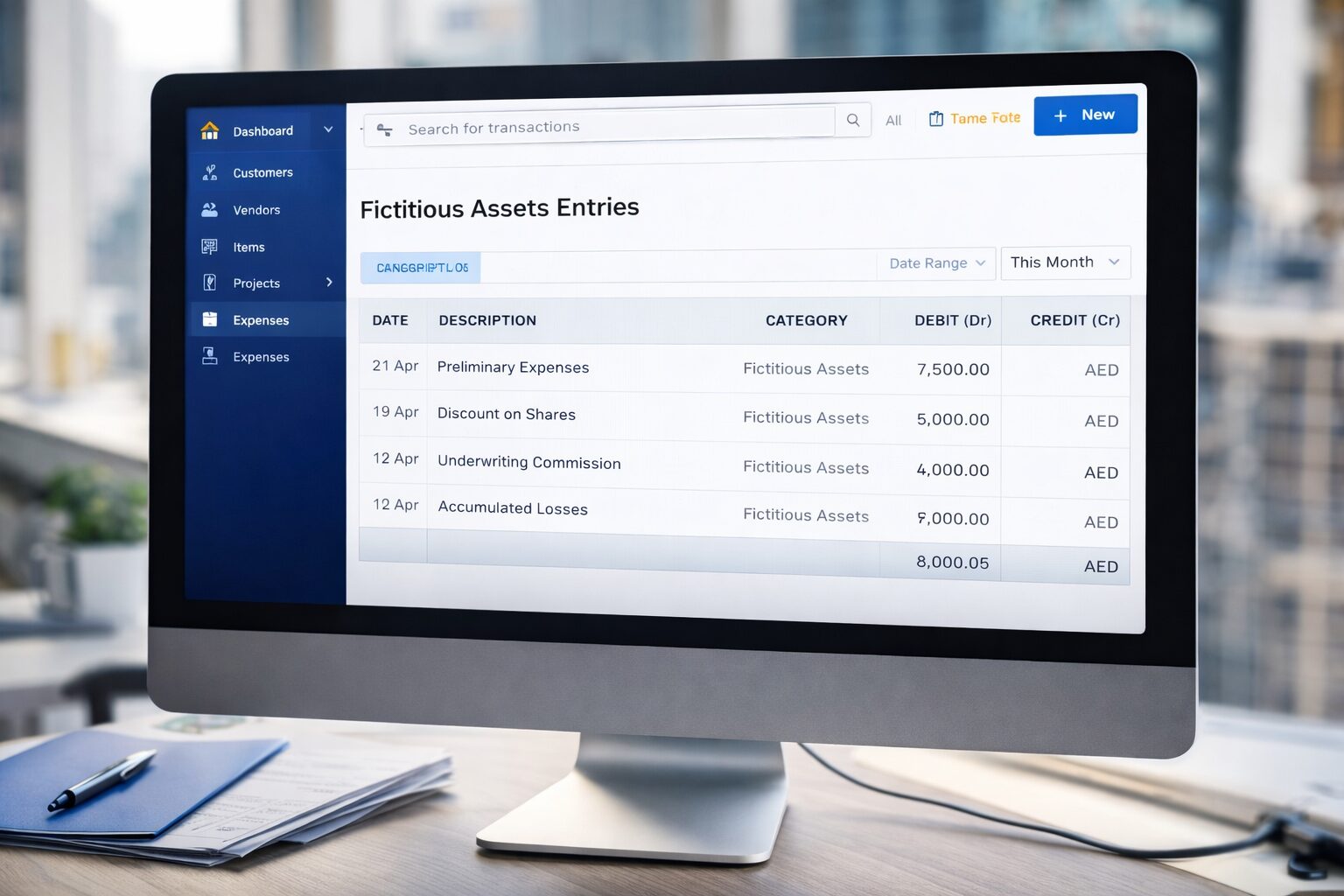

Preliminary Expenses

Costs incurred during company setup such as registration fees and legal charges.

Underwriting Commission

Fees paid to financial institutions when issuing shares.

Discount on Issue of Shares

Loss incurred when shares are issued below face value.

Accumulated Losses

Past losses carried forward instead of being fully written off.

How Are Fictitious Assets Treated Under IFRS in UAE?

Fictitious assets are generally not allowed under IFRS and should be expensed immediately.

IFRS focuses on showing only real assets that generate future economic benefits. Expenses like formation costs are usually charged directly to profit and loss.

Only specific items like development costs can be capitalized if they meet strict conditions.

Difference Between Fictitious Assets and Intangible Assets

| Feature | Fictitious Assets | Intangible Assets |

|---|---|---|

| Value | No real value | Has economic value |

| Examples | Preliminary expenses | Goodwill, patents |

| IFRS Treatment | Not allowed | Allowed |

| Nature | Deferred expenses | Real assets |

How to Write Off Fictitious Assets?

Writing off fictitious assets means transferring them to the profit and loss account.

- Identify the expense

- Follow IFRS rules

- Amortize or expense fully

- Update financial statements

Tools for Accounting and Compliance in UAE

Accounting tools help manage financial records and ensure compliance.

You can use tools like Tally, Zoho Books, or Odoo for managing expenses and reports.

What Should UAE Businesses Do Next?

Businesses should align accounting practices with IFRS standards.

- Review balance sheet

- Identify fictitious assets

- Consult accounting experts

- Update accounting systems

Conclusion

Fictitious assets are expenses carried forward without real value and should be treated carefully under modern accounting standards.

By following IFRS and proper accounting practices, UAE businesses can improve transparency, compliance, and financial reporting quality.